Icaza Provides Legal Advice to Creditors in US$1,050M Transaction

28/05/2026

Icaza, S.A. participates in WE LATAM

24/06/2026

Law No. 526 of May 28, 2026

The Republic of Panama enacted Law No. 526 of May 28, 2026, which introduces economic substance rules and requirements in Panama, applicable exclusively to entities that are members of Multinational Groups and that earn foreign-source passive income (the “Law”). This legislation will enter into force in the fiscal year 2027.

Below, we address the most relevant questions for individuals and organizations that own Panamanian companies or private interest foundations regarding the scope and application of this new law.

1. Scope of the Law

Who does this law apply to?

The Law applies to entities (companies or foundations) that: (i) are members of multinational groups, (ii) have been incorporated or are domiciled in Panama, and (iii) earn foreign-source passive income.

A multinational group is defined as a group of two or more entities, connected through ownership or control, which are tax residents in different jurisdictions, including the parent company, its subsidiaries, and permanent establishments.

Panamanian companies and foundations are not automatically considered tax residents in Panama merely by virtue of being incorporated in Panama. Rather, they are considered tax residents only if they have obtained a Tax Residency Certificate issued by Panama’s General Directorate of Revenue (Dirección General de Ingresos – DGI) after fulfilling all applicable requirements.

What types of income are considered foreign-source passive income?

The Law considers the following foreign-source income to be passive income:

- Dividends

- Interest

- Royalties

- Capital gains

- Real estate income

- Other foreign-source capital income

Does this apply to my company or foundation if it is not part of a multinational group?

No, even if your entity is incorporated in Panama and receives income from different countries, the Law applies exclusively to entities that are part of a multinational group.

If your structure consists of a Panamanian company or foundation that operates independently and is not connected to entities in other jurisdictions through common ownership or control, or is not part of a group of entities with tax residence in different jurisdictions, this Law does not apply directly to it, regardless of the sources of income received by the Panamanian entity.

What does “multinational group” mean?

A multinational group is a group of two or more entities connected through ownership or control and that are tax residents in different jurisdictions, including the parent company, subsidiaries, and permanent establishments.

Although this is not the only applicable criterion, an entity is generally considered part of a multinational group if it is included in the group’s consolidated financial statements or, even if excluded, should have been included in those consolidated financial statements.

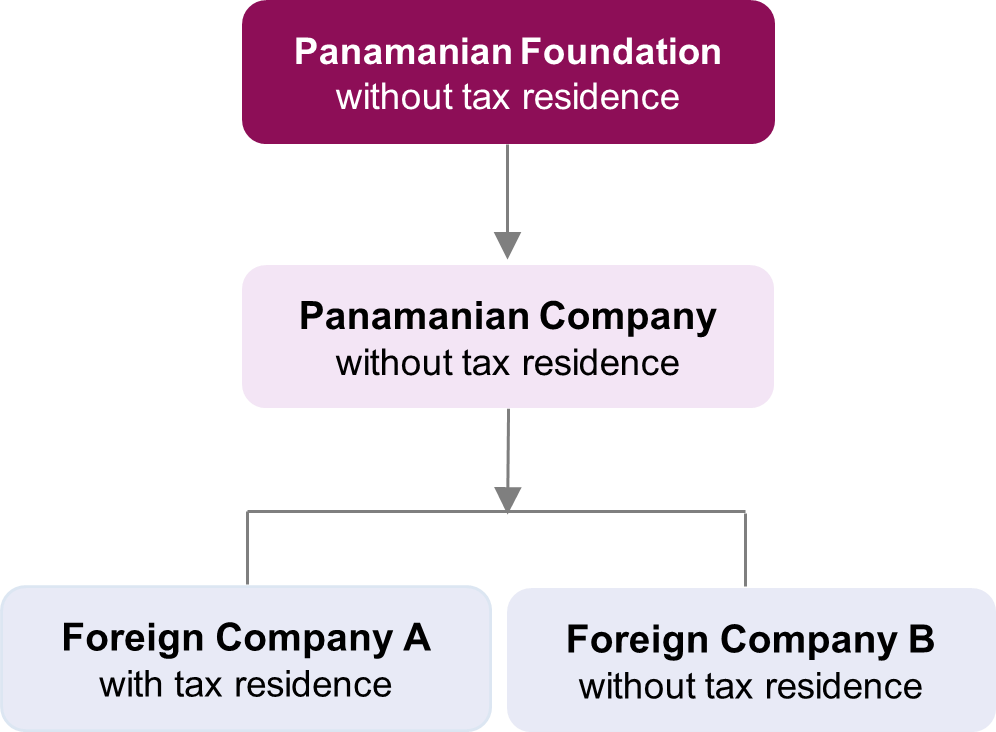

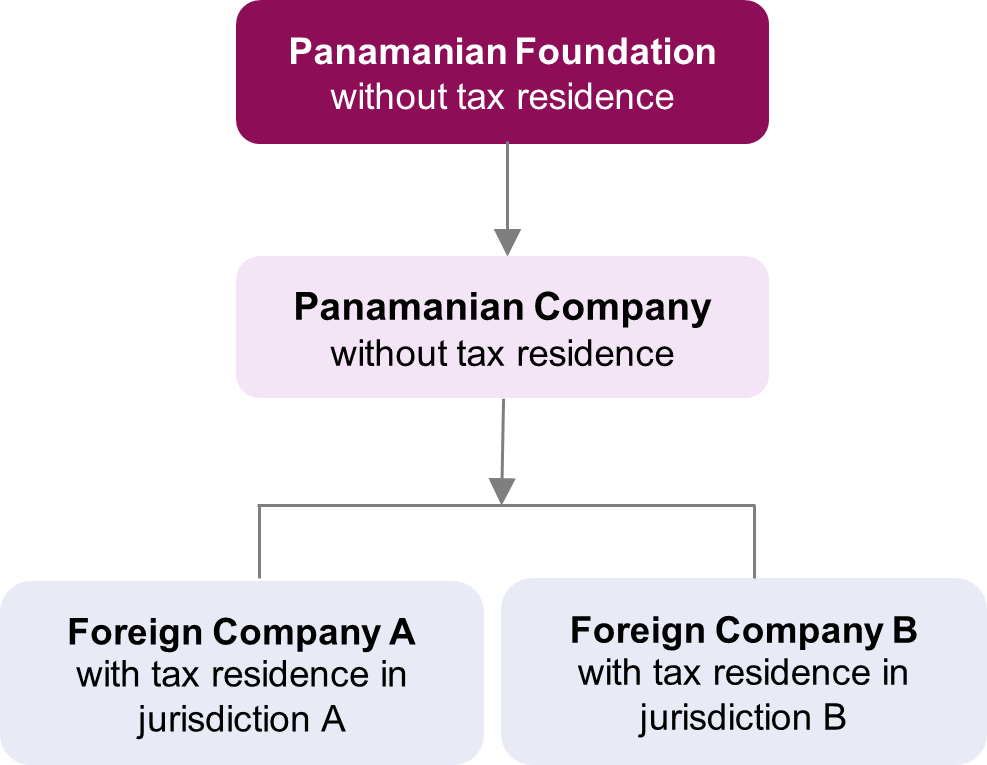

The following diagrams illustrate when a structure constitutes (or does not constitute) a multinational group:

It is not a Multinational Group

It is a Multinational Group

Note: The determination of whether a structure constitutes a multinational group does not change if the Panamanian Foundation is removed from the structures described above.

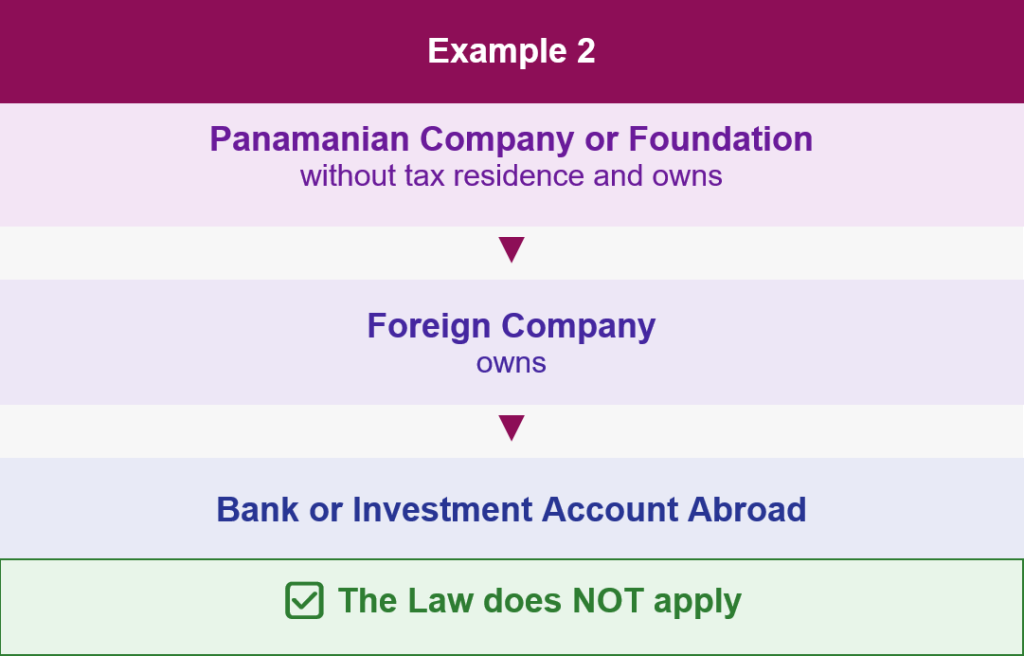

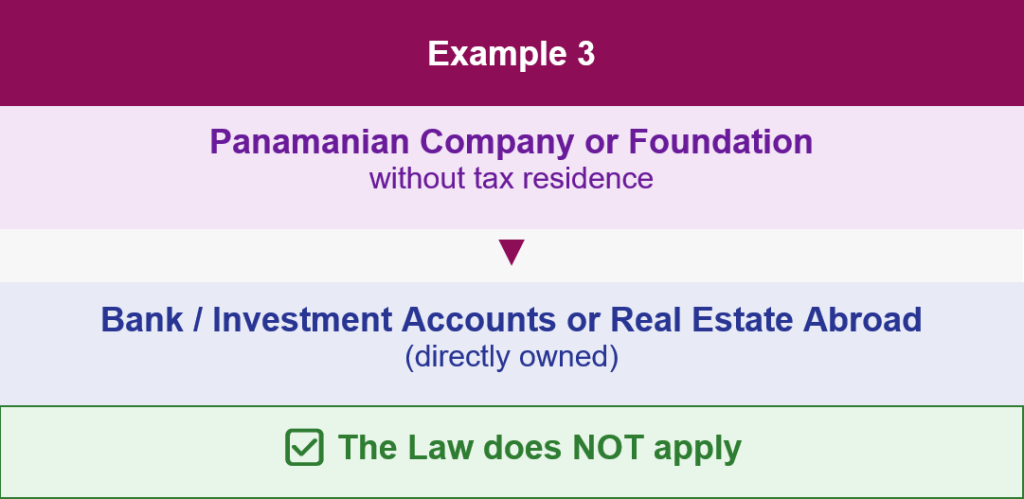

Below are practical examples where the Law does NOT apply:

2. General Principle and Economic Substance

What does it mean for income to be “non-taxable” under the territoriality principle?

Panama applies the territorial taxation principle, under which foreign-source income is not subject to income tax.

For Panamanian entities that are members of a multinational group, the Law maintains this principle, but subject to one condition: the entity wishing to benefit from it must demonstrate that it has real economic substance in Panama.

What is required to demonstrate economic substance?

The Panamanian entity must comply with the following requirements:

- Maintain adequate human resources, appropriately compensated and suitably qualified, dedicated to the principal activities referred to in the Law, including the generation, administration, management and/or control of assets that produce foreign-source income.

- Have adequate facilities in Panama for carrying out the principal activities associated with such assets.

- Make the strategic decisions necessary for its operations and assume related risks from within Panamanian territory.

- Incur operating costs and expenses in Panama, in addition to personnel and facility-related expenses, that are appropriate considering the activities carried out in Panama.

Can an entity outsource its activities and still meet the substance requirements?

Yes, the Law allows entities to engage third parties in Panama to perform the principal activities, provided that such activities are effectively carried out in Panama and remain under the direct supervision and control of the contracting entity. Responsibility cannot be delegated, the entity must remain in charge of the activities.

3. Excluded Entities

Are there entities excluded from the regime even if they belong to a multinational group?

Yes, subject to the conditions established in the Law, the following categories are expressly excluded:

- Regulated banking and financial institutions

- Insurance and reinsurance companies

- Securities market intermediaries

- Investment fund and pension fund managers

- Entities engaged in the commercial operation of vessels registered under the Panamanian flag, including shipowners as well as vessel operators and managers

4. Consequences of Non-Compliance

What happens if my entity fails to demonstrate economic substance?

A Panamanian entity that is part of a multinational group will be classified as a “non-qualified entity.” In such case, its foreign-source passive income will be subject to a single and final tax rate of 15% on the taxable net income of the relevant fiscal period.

Are there additional penalties beyond the 15% tax?

Yes, in addition to the 15% tax, non-compliance may result in the application of fines, surcharges, and interest in accordance with the Panamanian Tax Code.

What is the Anti-Abuse Clause?

The Ministry of Economy and Finance (MEF) has the authority to disregard structures or arrangements whose principal purpose is to obtain tax benefits that are inconsistent with the purpose of the Law. This means that purely formal or artificial structures lacking real economic substance may be ignored, resulting in the relevant Panamanian entity being subject to the tax treatment applicable to a non-qualified entity.

5. Income Tax Return filing obligation for entities that are members of a multinational group

What additional obligation will apply to my company or foundation if it belongs to a multinational group?

In addition to demonstrating economic substance in Panama, Panamanian entities that are members of a multinational group will be required to submit an annual sworn income tax return within the deadlines established by law to demonstrate compliance with the economic substance requirements. This requirement applies to entities that earn both Panamanian-source income and foreign-source passive income, as well as those that earn exclusively foreign-source passive income. ,

6. Effective Date and Key Deadlines

When does this law take effect?

The law shall enter into force in the fiscal year 2027.

Is there a deadline for the government to issue implementing regulations?

Yes, the Executive Branch has a maximum period of 90 calendar days from the promulgation (publication in the Official Gazette) of the Law to issue the corresponding regulations. The promulgation of the Law occurred on May 28th, 2026.